How to Manage Overfitting

Wikipedia provides this definition:

Overfitting occurs when a statistical model describes random error or noise instead of the underlying relationship.

In trading, this means creating a strategy that fits past noise perfectly but has no predictive power going forward. It is one of the most dangerous pitfalls in systematic trading.

The Problem with Over-Optimization

When traders use a single dataset to optimize multiple parameters — such as stop loss and take profit levels — their model risks losing its trend-following ability and instead captures random market noise.

The result is an equity curve that looks beautiful on the optimization dataset but falls apart on new data.

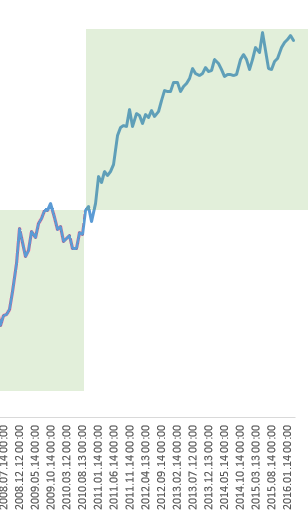

Here is an 8-year backtest showing impressive results:

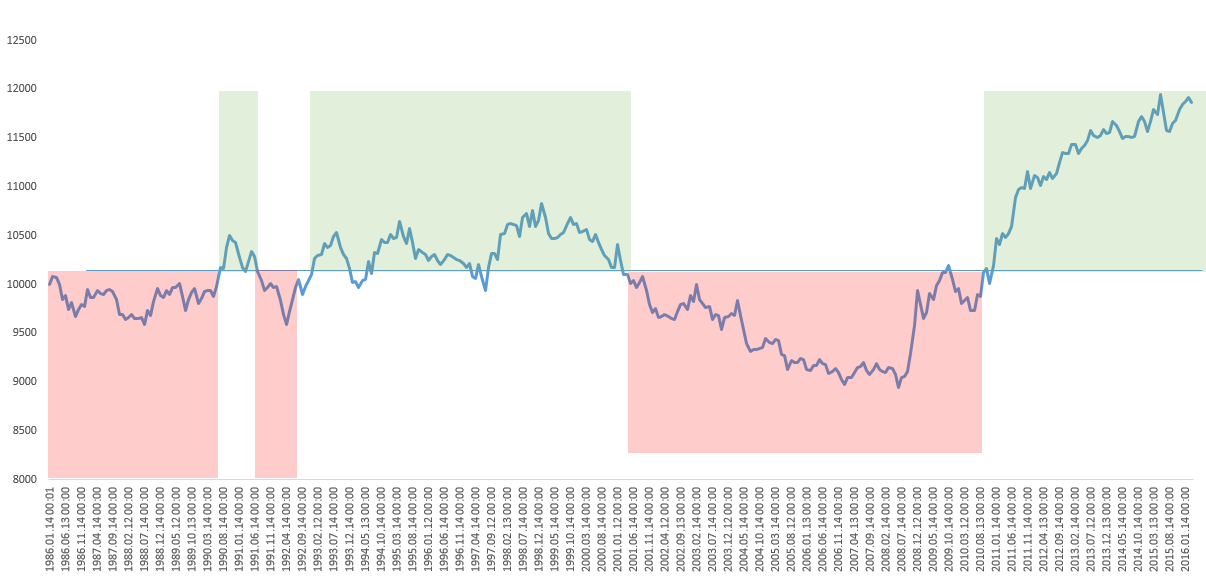

And here is the same strategy tested over 40 years of data:

The dramatic difference between the two charts reveals that the 8-year optimization was capturing noise, not a real market edge.

The Validation Methodology

Here is the approach I recommend to detect and avoid overfitting:

Step 1 — Develop the basic concept

Start with a simple strategy idea. Use a 10-year historical dataset with minimal parameters (ideally just stop loss and entry condition). Never optimize aggressively on the development set.

Step 2 — Optimize conservatively

If the strategy is profitable on the initial dataset, optimize using as few parameters as possible. Each additional parameter requires more data to be statistically valid.

Step 3 — Validate on 30+ years

Take the optimized parameters and test them on previously untouched data — at least 30 years of history, covering different market regimes.

Step 4 — Interpret the outcomes

When testing against the extended dataset, you will encounter one of three outcomes:

- Continued profitability → The model captures a genuine market behavior. High confidence.

- Flat performance → Market behavior shows randomness relative to your entry. The pattern may not be real.

- Losses → An underlying behavior existed in the short window but has since changed. Investigate why.

Conclusion

The less your trading system's performance is sensitive to small parameter changes, the stronger it is. Successful algorithmic trading requires:

- A genuine statistical edge (not noise)

- Conservative parameter optimization

- Validation on out-of-sample data spanning multiple market regimes

Avoid overoptimization. Prioritize finding underlying market behavior patterns over fitting noise to produce a prettier backtest.